Can Banks Close Accounts for OnlyFans Income? Explanation

If you earn money on OnlyFans, it’s normal to worry: “Can my bank shut me down for this?” The honest answer is yes, a bank can close (or restrict) an account...

If you earn money on OnlyFans, it’s normal to worry: “Can my bank shut me down for this?” The honest answer is yes, a bank can close (or restrict) an account even if your income is legal, and even if you did nothing “wrong.” But it doesn’t happen to everyone, and there are practical steps you can take to reduce the risk and protect your cash flow.

This guide explains why account closures happen, what behaviors trigger scrutiny, and how to set up your banking so a single decision doesn’t derail your income.

This is educational, not legal, financial, or tax advice. Bank policies and laws change. Always verify with your bank and, if needed, a qualified professional.

Can banks close accounts for OnlyFans income?

Yes. Most banks reserve the right to close an account “at their discretion” (often with limited explanation) based on their internal risk policies and their account terms.

That does not mean OnlyFans income is automatically “bannable” at every bank. In practice, closures tend to happen when something about your account looks high-risk to compliance systems, or when your bank has a conservative approach to adult-industry payments.

The key idea: banks don’t only look at legality, they look at risk (fraud risk, chargeback patterns, identity mismatches, unusual activity, and reputational or policy risk).

Why banks sometimes close accounts (in plain English)

Banks operate under anti-money laundering (AML) and “Know Your Customer” (KYC) expectations, and they run automated monitoring on transactions. If the bank can’t get comfortable with what’s happening, they may choose to “de-risk” by ending the relationship.

Common reasons include:

1) The bank’s internal “high-risk” categories

Some banks classify certain industries as higher risk, including adult entertainment, due to:

- Higher fraud attempts in the ecosystem (not necessarily from you, but in general)

- Higher likelihood of disputes and refund friction in some adult-adjacent payment flows

- More frequent identity, privacy, and safety concerns (impersonation, doxxing, etc.)

Even if your activity is legitimate, a conservative bank may decide it’s not worth the compliance overhead.

2) Unusual transaction patterns that trigger monitoring

Banks look for patterns like:

- A sudden spike in deposits (for example, you go from $400/month to $9,000/month fast)

- Lots of small incoming transfers followed by immediate withdrawals

- Repeated failed payments or reversals

- Frequent international wires or unexpected intermediaries

Growth is not a problem by itself. The problem is growth that looks “unexplained” compared to the profile you opened the account with.

3) Name/KYC mismatch issues

If payouts don’t match the legal name on your bank account, or your bank thinks a third party is involved, it can trigger questions.

This can happen innocently, for example:

- Your payout profile uses a slightly different legal name than your bank record

- Your payout arrives with a descriptor tied to a parent company or payment processor name, and your bank can’t reconcile it quickly

4) Using products that prohibit adult income

Some consumer payment apps, prepaid services, or “personal only” accounts may have rules about business use or certain industries.

This is where creators get caught without realizing it: it’s not always about OnlyFans itself, it’s about using the wrong financial product for business income.

For an overview of AML expectations in the US, you can read FinCEN’s basic resources on the Bank Secrecy Act.

What increases your risk (and what doesn’t)

Let’s separate myths from reality.

Higher-risk situations

These scenarios tend to increase the chances of friction:

- You run all payouts into your “life account” (rent, family transfers, side gigs, everything mixed together)

- You can’t quickly document what the income is from if the bank asks

- You move money in and out the same day like clockwork

- You use an account type that forbids business activity

- You have frequent chargeback-like behavior in adjacent services (not usually OnlyFans payouts, but other linked activity)

Lower-risk situations

These usually make your banking look cleaner and easier to understand:

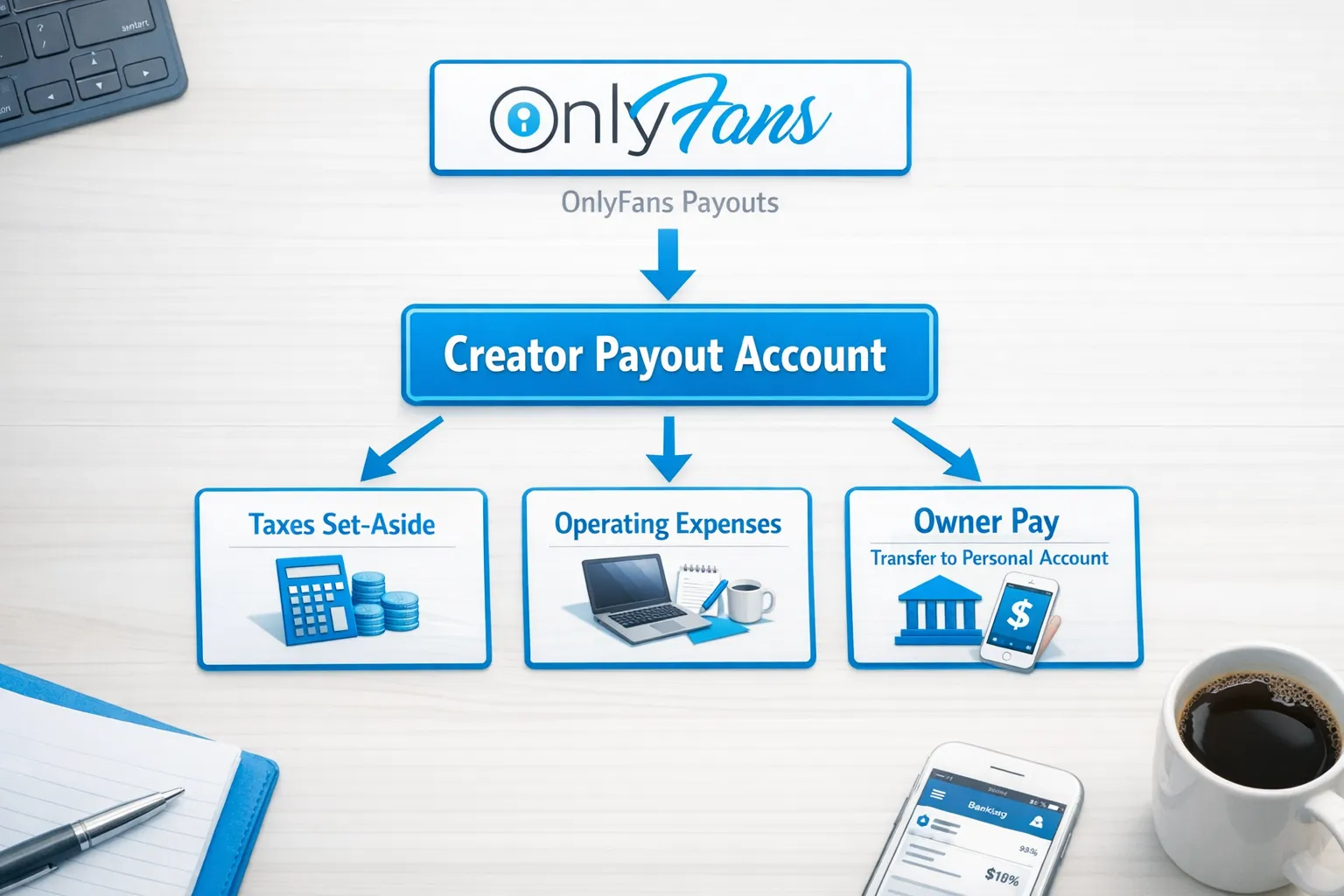

- A dedicated account used only for creator payouts and business expenses

- Consistent payout schedule (weekly or biweekly) and consistent transfer routine

- Clear records (payout statements, invoices/receipts, tax tracking)

- Correct name matching across all payout settings

If you want a simple money routine that keeps your records bank-friendly and tax-friendly, this pairs well with Lookstars’ bookkeeping habit guide: OnlyFans Taxes: Weekly Habit to Stay Organized.

A safer banking setup: a simple decision framework

If you’re deciding how to structure your accounts, use this “risk-first” framework:

Step 1: What’s your privacy goal?

- If privacy is a major concern, you’ll likely want separation (so your main household account does not show creator-related deposits).

- If privacy is less critical, separation still helps for bookkeeping and bank clarity.

(Privacy also includes digital footprint, not just bank statements. If you’re trying to stay anonymous from friends or family, this guide helps: How to Secretly Promote Your OnlyFans (Without Friends or Family Finding Out).)

Step 2: How consistent is your income?

- If you’re early-stage or inconsistent, a dedicated personal account might be enough.

- If you’re consistent and scaling, it may be time to treat it like a business operation (including account type and documentation).

Step 3: Do you need an LLC (or business entity)?

An LLC can help with separation and operations, but it’s not a magic shield and doesn’t guarantee privacy or bank acceptance.

If you’re considering it, read: LLC for OnlyFans: When It Makes Sense.

Banking options compared (practical pros and cons)

Here’s a realistic comparison you can use to choose a setup.

| Option | Best for | Pros | Cons / risks | What to do to make it safer |

|---|---|---|---|---|

| Single personal checking account (everything mixed) | Very early stage, very small volume | Simple | Harder to explain patterns, privacy exposure, messy bookkeeping | If you insist on this, at least track payouts and taxes weekly |

| Dedicated personal account for payouts only | Most creators starting to scale | Cleaner transactions, better privacy, easier documentation | Still “personal” product rules may limit business use at some banks | Ask the bank if creator income is acceptable; keep documentation ready |

| Business account (sole prop or LLC) | Consistent income, hiring help, treating it as a real business | Clear separation, often better support for business activity | More setup, more paperwork, still not a guarantee | Keep entity docs, contracts, and clean bookkeeping |

| Multi-currency/fintech account (where available) | International creators, frequent currency conversion | Can reduce payout friction in some cases | Product rules vary, support quality varies | Confirm acceptable use and keep matching KYC info |

No setup eliminates risk 100%. The goal is to make your financial life clean, explainable, and resilient.

What to do today to reduce your risk (quick checklist)

If you want the “do this now” version, here it is.

- Open a dedicated payout account (personal or business) used only for creator income and related expenses.

- Make sure your legal name matches exactly across your bank, your payout settings, and any tax records.

- Build a simple documentation folder (digital is fine): payout statements, invoices/receipts for business expenses, and your tracking spreadsheet.

- Avoid “in and out” behavior (for example, receiving payouts and instantly draining the account every time).

- Set a predictable transfer routine: pay yourself a consistent “owner pay” amount weekly or twice monthly.

If you’re dealing with delays or failed payouts on the bank side, this troubleshooting guide can help you separate bank issues from platform issues: International Payouts: How to Avoid Common Delays.

A copy/paste script to ask your bank (without oversharing)

You do not need to be graphic. You do need to be honest.

Here’s a script you can use by phone or secure message:

“Hi, I receive income from an online subscription content platform where I’m a verified creator. Payments are sent to me as payouts. Can you confirm this type of income is acceptable under your account terms? If needed, I can provide payout statements and tax documentation.”

If they ask what platform, answer truthfully. If you’re not comfortable naming it on a first message, you can ask what documentation they need to classify the income source.

What not to say (because it can backfire)

- Don’t claim it’s “gifts” or “friends sending money” if it’s business income.

- Don’t route income through an app whose terms prohibit adult work or business use.

- Don’t open accounts with inaccurate information.

Those shortcuts often create the exact compliance flags you’re trying to avoid.

If your bank closes your account: what happens next?

First, breathe. A closure is stressful, but it’s usually solvable.

Here’s the practical response plan:

1) Get clarity on timelines and access to funds

Ask:

- When will the account be restricted or closed?

- Will funds be mailed by check, transferred, or held for a period?

- What documents can you provide confirming closure and remaining balance?

Banks sometimes limit details, but you can still get the operational facts.

2) Stop future payouts from landing there

Update your payout method on OnlyFans as soon as you have an alternative account ready.

If you’re mid-payout cycle, avoid repeated rapid changes. Make one clean change, then document it.

3) Preserve your records

Download or export:

- Bank statements showing incoming payouts

- Any closure notices

- Your payout history from the platform

This is useful for taxes, disputes, and explaining income to a new bank if needed.

4) Choose a more resilient setup going forward

This is where the “dedicated payout account” strategy matters. If your creator account is separated, a closure doesn’t freeze your rent money.

Who is most likely to run into banking issues?

This section is here to be honest, not scary.

You’re more likely to experience friction if:

- Your income jumps fast and your financial profile doesn’t match (for example, student account activity suddenly becomes high-volume business deposits)

- You’re international and dealing with intermediaries, currency conversions, or inconsistent bank routing

- You’re mixing multiple income streams without tracking (brand deals, cash, multiple platforms)

You’re less likely to experience major issues if:

- You run your creator work like a business (separation, documentation, predictable transfers)

- You keep your identity and KYC info consistent everywhere

Where an OnlyFans management agency fits (and where it doesn’t)

A management team can’t force a bank to keep an account open. But a good OnlyFans management agency can reduce the chaos that triggers problems in the first place.

For example, Lookstars helps creators stabilize operations through:

- Structured posting and revenue systems (so deposits look consistent, not random)

- Strong fan monetization (so you rely less on constant banking gymnastics)

- Privacy protection tools like country blocking guidance and security setup

- Content leak protection workflows (which reduces panic-driven financial moves after leaks)

If you’re currently doing everything alone, you may also like: Working With an Agency vs Running OnlyFans Alone.

Frequently Asked Questions

Can a bank close my account without telling me why? Yes, sometimes. Many banks limit what they disclose for security and compliance reasons. You can still ask about timelines, fund access, and what documentation they can provide.

Will my bank statement show “OnlyFans”? Sometimes statements show the platform name, sometimes a parent company or payment processor descriptor. It varies by bank and payout routing. If privacy is important, use a dedicated payout account.

Should I open a business bank account for OnlyFans income? It can help with separation and professionalism if your income is consistent or you’re hiring help, but it’s not a guarantee. The safest move for most creators is at least a dedicated payout account plus clean records.

Does forming an LLC prevent bank problems? Not automatically. An LLC can improve separation and operations, but banks still apply risk policies. If you form one, keep your KYC, paperwork, and bookkeeping tight.

What should I do if my bank freezes funds from payouts? Ask for the timeline and required documentation, keep communication calm and professional, and preserve all payout statements and bank notices. If it’s urgent, consult a qualified professional for guidance based on your country.

Is it safer to use multiple platforms so I’m not dependent on one payout stream? Diversification can reduce income risk, but it adds operational complexity. If you expand, track payouts carefully and keep accounts organized.

Want a more stable, privacy-first creator setup?

If you’re building real income on OnlyFans, the goal is not just “make more,” it’s keep it predictable and protectable.

Lookstars is a full-service OnlyFans management agency that supports creators with marketing, fan engagement, posting strategy, privacy protection, and content leak protection, with no upfront costs and flexible, cancel-anytime contracts.

If you want help building a cleaner operation (so your income is easier to manage and less stressful to maintain), you can learn more at Lookstars Agency.

Ready to transform your career?

Join hundreds of creators already earning six figures with Lookstars Agency.

Share this article

Best OnlyFans Agency

Europe's Leading OnlyFans Management Agency.

100% Free Ebook

Get our guide and unlock the secrets to OnlyFans success.

100% Free Ebook

Get our guide and unlock the secrets to OnlyFans success.

Free Revenue Calculator & Profile Analyzer

Try them for freeContinue reading...

Am I Attractive Enough for an OnlyFans Agency? The Answer

Can You Ever Fully Delete Your OnlyFans Content? The Reality